Deferred tax Basic for your ACCA:

- Timing Difference: Deferred tax arises from differences in the timing of when expenses are recognized for accounting and tax purposes.

- Accounting vs. Tax: Accounting rules and tax laws may treat expenses differently.

- Example: Depreciation: A common example is depreciation of assets.

- Temporary Difference: The difference in how an item is treated for accounting and tax creates a "temporary difference."

- Future Tax Liability: If you deduct more for tax purposes earlier, you'll owe more taxes later.

- Deferred Tax Liability: This future tax obligation is recorded as a "deferred tax liability" on your financial statements.

- "I Owe You" for Taxes: Essentially, it's like setting aside money for taxes you'll pay in the future.

- Matching Accounting and Tax: This helps align your financial reporting with your tax obligations.

- Future Tax Impact: Reflects the future tax consequences of current accounting decisions.

- Key Concept: Deferred tax is a fundamental concept in financial accounting that helps ensure accurate financial reporting.

Core Concept: Deferred tax arises because accounting profit (used for financial reporting) and taxable profit (used for tax calculations) are often different. This difference is due to timing differences in when revenues and expenses are recognized.

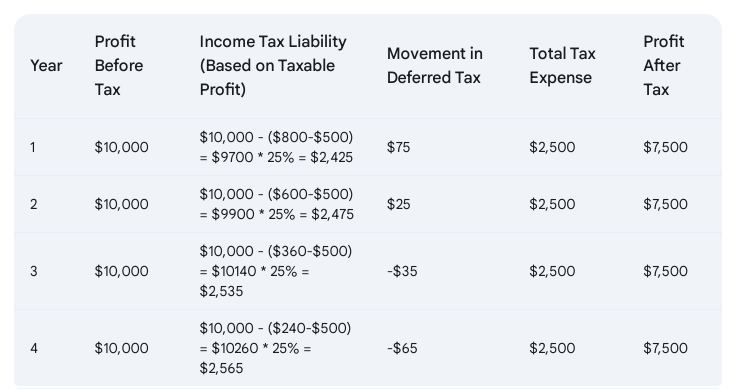

Example 1

The core example uses an asset costing $2,000, depreciated straight-line over 4 years ($500 per year), and capital allowances (tax depreciation) as follows:

Year 1: $800

Year 2: $600

Year 3: $360

Year 4: $240

Tax Rate: 25%

Solution:

As shown in the table, a deferred tax liability of $75 is recognized in Year 1 and $25 in Year 2. In Years 3 and 4, a deferred tax asset is recognized due to the negative taxable income difference.

Overall Impact:

The deferred tax liability recognized in the earlier years will eventually be settled in the later years when the higher taxable income is recognized. This ensures that the appropriate amount of tax is paid over the asset's useful life, even though the timing of tax payments may differ from the timing of accounting income recognition.

By recognizing deferred tax liabilities and assets, companies can provide a more accurate picture of their financial performance and position by reflecting the future tax consequences of timing differences between accounting income and taxable income.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

No comments: